On 2 April 2025, US President Donald Trump signed an executive order and announced that reciprocal tariffs will be imposed on global trade partners. The increase in tariff rates exceeded market expectations. While it was not surprising that a basic tariff rate of 10% was imposed on all countries and regions exporting to the US, higher rates were applied to countries and regions with significant import volumes, resulting in an estimated effective tariff rate of around 12-18% from the perspective of the US public.

The Nikkei Stock Average declined following the announcement. However, since there were no additional tariffs on items like automobiles, and considering the previous market declines, the market may have already experienced the worst for the moment. The focus will now shift to companies expanding production in the US and negotiations involving Japan importing Alaskan natural gas and US defence equipment. These developments could play a role in the effective reduction of tariff rates in the future.

Another focal point is the extent to which the tariff rate increases (which are not necessarily supported by all Americans) impact consumer sentiment by accelerating consumption, inducing supply shortages, and causing the stockpiling of raw materials by manufacturers and importers. Market view is divided on whether consumers will reduce consumption to save due to future uncertainty, potentially leading to a downturn in the economy, or if they will maintain consumption by reducing savings, potentially resulting in labour shortages, wage increases, and increased inflation. Market sentiment suggests that if the former scenario occurs, the Federal Reserve may lower interest rates sooner, while if the latter scenario unfolds, it may do so later.

Given that on 3 April the yen strengthened and the dollar weakened, and that US long-term interest rates declined during the Asian trading hours, the market seems to be more concerned about the economic downturn than inflation from the latter scenario mentioned above. Over the next few months, as the impact of the tariff rate increases intensifies, the market is likely to closely monitor consumption-related statistics amid fears of further deterioration in consumer spending.

Looking ahead, the Trump administration could change its policies towards the second half of the year as it begins focusing on next year’s midterm elections. This could result in the following:

- US consumption may not deteriorate as much as feared

- The semiconductor industry could retain is long-term growth trajectory

As such, despite current concerns, the markets could recover towards the end of the year. The Dow Jones Industrial Average is forecast to be around 46,000 and the Nikkei Stock Average is expected to be around 41,000 yen in March 2026.

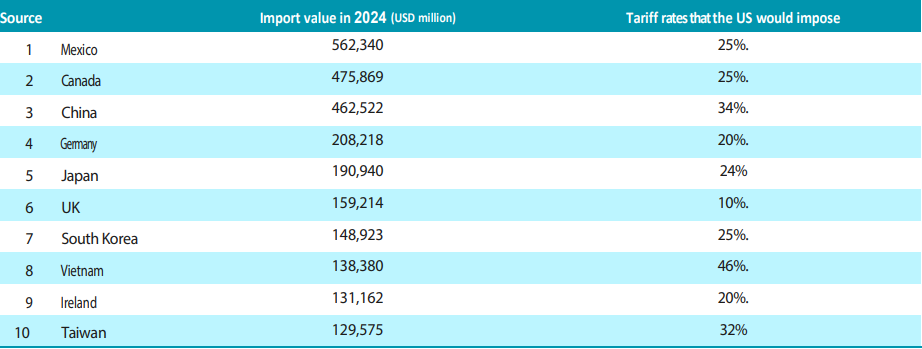

Top 10 sources of US imports by value and tariff rates to be imposed

Source: US Department of Commerce and information deemed reliable